Introduction to the Mortgage Process for Lenders

The mortgage process can be a complex maze for both borrowers and lenders, with multiple steps and numerous variables involved. For lenders, understanding each stage of this process is crucial to not only streamline operations but also to enhance customer satisfaction and maintain compliance with regulations. This guide aims to unravel the mortgage process for lenders, offering valuable insights into each critical phase and sharing best practices to ensure a smooth transaction. By mastering the intricacies of the mortgage process for lenders, lending professionals can facilitate better decisions and provide superior service.

Understanding Key Terms and Concepts

Before diving into the process itself, it’s essential for lenders to have a firm grasp of key terms and concepts that frequently arise during mortgage transactions. Key terms include:

- APR (Annual Percentage Rate): The total yearly cost of a mortgage loan expressed as a percentage of the loan amount.

- Loan-to-Value Ratio (LTV): The ratio of the loan amount to the appraised value of the property, which helps assess risk.

- Debt-to-Income Ratio (DTI): A measure of an individual’s monthly debt payments relative to their monthly income, critical in evaluating creditworthiness.

- Pre-approval: A lender’s readiness to provide a mortgage based on the borrower’s creditworthiness and financial status, often involving a rigorous assessment of financial documentation.

- Underwriting: The process of assessing risk and determining the loan amount a borrower qualifies for, which includes a review of financial statements, credit history, and property information.

A robust understanding of these terms not only allows lenders to communicate effectively with clients but also aids in complying with various regulatory standards.

The Importance of Efficient Workflow

In the mortgage industry, time is of the essence. An effective workflow can significantly increase efficiency and lead to quicker loan turnarounds. This improvement not only enhances the lending experience for borrowers but also boosts the lender’s competitive edge. Implementing systems such as automated loan processing, extensive use of digital submissions, and clear communication protocols contributes to a more streamlined mortgage process.

Moreover, adopting a technology-driven approach ensures that lenders can maintain accuracy and track each stage of the loan process, which is essential for compliance and operational excellence.

Initial Steps for Lenders in the Process

The mortgage process begins even before a borrower applies for a loan. Lenders must establish effective marketing strategies and build relationships with potential borrowers. This groundwork can include:

- Developing educational content that informs potential borrowers about the mortgage process.

- Engaging in community outreach programs to build rapport and trust.

- Leveraging social media channels to connect with potential clients and real estate agents.

By fostering relationships and providing valuable educational material, lenders can create a pipeline of pre-qualified borrowers ready to engage in the mortgage process.

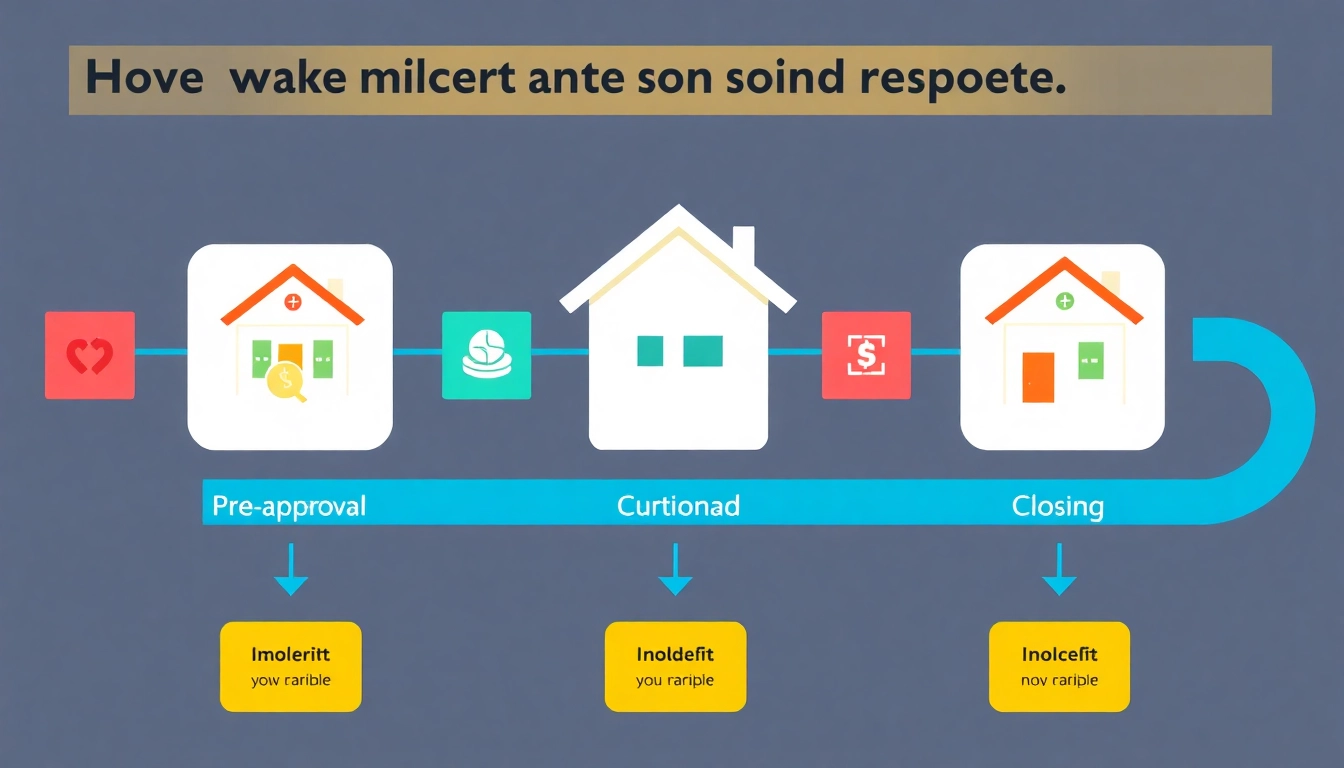

Step 1: Getting Pre-Approved

What is Pre-Approval?

Pre-approval is a critical first step in the mortgage process. It involves evaluating a borrower’s financial history, income, assets, and liabilities to determine their eligibility for a loan. This step sets the groundwork for a smoother mortgage transaction down the line.

For lenders, offering pre-approval services enhances customer satisfaction by allowing borrowers to understand their borrowing capacity, thus making informed decisions when purchasing a home. It signifies a commitment from the lender and can be an essential marketing tool.

Documentation Required for Pre-Approval

To facilitate pre-approval, lenders need certain documentation which generally includes:

- Proof of income (usually the last two years of W-2 forms or pay stubs).

- Bank statements for the last three to six months.

- Tax returns for the past two years.

- Details on any other additional income, assets, or debts.

Being thorough in gathering this information can expedite the pre-approval process and enhance the borrower’s confidence in moving forward.

Common Challenges Lenders Face

While pre-approval is a vital step, it is not without its challenges. Common obstacles may include:

- Incomplete documentation from the borrower.

- Credit issues that arise once a credit report is pulled.

- Misunderstandings regarding financial jargon that can lead to confusion and delays.

Addressing these challenges requires open communication and proactive problem-solving. Educating borrowers about documentation requirements beforehand can alleviate many issues.

Step 2: Application Submission

Collecting Necessary Information

Once pre-approved, borrowers will formally submit their applications. For lenders, this is the stage where comprehensive information collection is critical. Lenders should gather:

- Complete application forms with personal and financial information.

- Documentation of employment history.

- Asset verification documents.

- Any additional documents pertinent to the transaction, such as purchase agreements.

Implementing an organized checklist for both lenders and borrowers can ensure that nothing is overlooked, paving the way for a smoother processing phase.

How to Verify Applicant Data

Data verification is a fundamental element of the mortgage application process. Lenders should meticulously validate borrower information through:

- Contacting employers to confirm employment statuses.

- Utilizing services that provide comprehensive credit reports.

- Checking financial documents against original sources to ensure authenticity.

Thorough verification reduces the risk of fraud and provides a clearer picture of the borrower’s financial health, aiding in informed lending decisions.

Best Practices for Application Handling

Efficient application handling is of paramount importance to avoid misunderstandings and rework. Best practices include:

- Providing clear instructions to borrowers about required documentation.

- Utilizing digital tools that allow for the seamless upload and tracking of documents.

- Establishing a robust communication system to keep borrowers updated on the application status.

By adopting these practices, lenders can build trust with borrowers and enhance the overall satisfaction with the mortgage process.

Step 3: Loan Processing

Critical Role of Underwriting

Loan processing leads directly to underwriting, which is one of the most critical steps in determining whether a loan will be approved or denied. Underwriters assess all aspects of the borrower’s financial history and the property itself. Key considerations during underwriting include:

- Analyzing the borrower’s credit score and history.

- Ensuring that the LTV and DTI ratios meet the lender’s criteria.

- Reviewing the appraisal report to confirm property value.

Successful underwriting culminates in a formal loan decision, with conditions outlined for clear communication back to both lenders and borrowers.

Timeline Expectations

Lenders should set realistic expectations for their clients regarding timelines. On average, obtaining a mortgage can take anywhere from 30 to 60 days, depending on various factors such as:

- The complexity of the borrower’s financial situation.

- Availability of required documentation.

- The efficiency of communication among all parties involved.

By informing borrowers about these potential timelines, lenders can manage expectations and reduce anxiety during the process.

Technology’s Impact on Processing

Incorporating technology in loan processing enhances speed and accuracy. Tools like automated underwriting systems and digital document management allow lenders to:

- Serve multiple clients simultaneously.

- Minimize human error during data entry.

- Track applications more efficiently through the pipeline.

Using technology not only streamlines operations but also improves the overall customer experience.

Step 4: Closing the Mortgage

Documents Required at Closing

The closing phase brings together all parties involved in the transaction to finalize the mortgage. Lenders must ensure that the following documents are ready:

- The Closing Disclosure, which outlines the loan terms and final costs.

- Updated title reports that confirm ownership and any encumbrances.

- Loan agreement documents that the borrower must sign.

Providing a detailed list of required documents to the borrower increases transparency and allows for a smoother closing process.

Ensuring a Smooth Closing Process

To ensure a seamless closing, lenders should:

- Communicate clearly with all parties involved, including real estate agents and title companies.

- Prepare for potential last-minute issues by conducting thorough pre-closing checks.

- Foster an environment of collaboration to address any concerns promptly.

By streamlining communication and anticipating challenges, lenders can significantly enhance client satisfaction during this critical stage.

Post-Closing Follow-Up for Lenders

The interaction between lenders and borrowers doesn’t end at closing. Following up can provide valuable insights into the client’s experience. This post-closing engagement can include:

- Surveys to gather feedback.

- Information on loan servicing and payment options.

- Updates on potential refinancing opportunities in the future.

Post-closing follow-ups not only show commitment to borrower satisfaction but can also foster long-term relationships that lead to referrals and additional business.